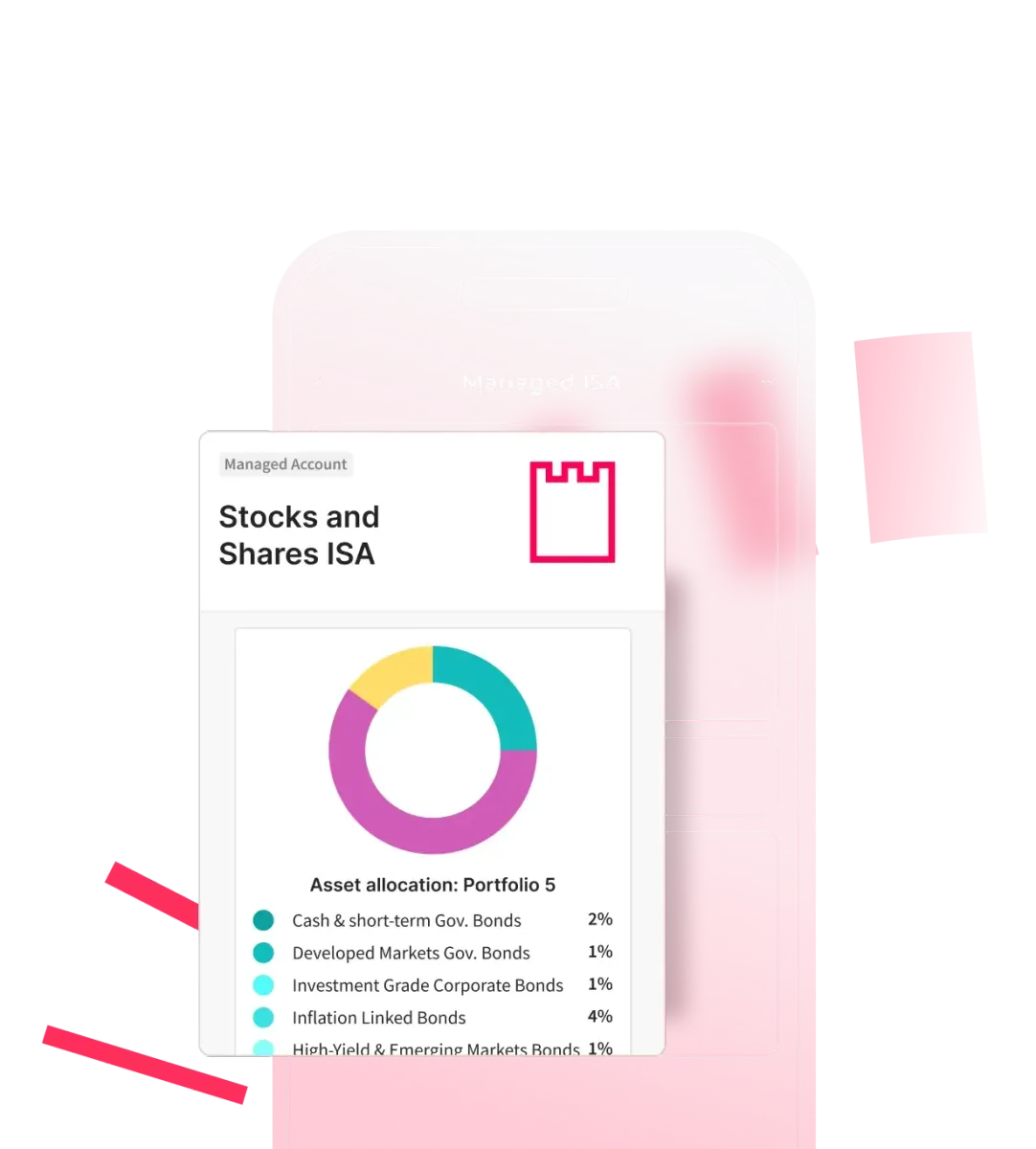

Managed Stocks and Shares ISA.

Unlock the full potential of your wealth with a Managed Stocks & Shares ISA. Our investment experts manage and monitor your investments, giving your wealth the best chance to grow.

Unlock the full potential of your wealth with a Managed Stocks & Shares ISA. Our investment experts manage and monitor your investments, giving your wealth the best chance to grow.

Investments can go down in value as well as up, and you may get back less than you put in. See our full risk disclosure for details.

A globally diversified portfolio matched to your goals and personal risk profile, backed by smart technology and human expertise.

Our Asset Allocation team monitors and regularly rebalances your ISA to maintain its optimal structure.

Your ISA portfolio stays aligned with your personal risk profile and investment goals.

Cutting-edge technology drives in-depth analysis for strategic investment decisions.

Open communication keeps you engaged and in the loop about your ISA investments.

Our Managed ISA can be personalised with different investment styles to align with your values and goals.

Choose a diversified portfolio with a mix of assets that meet environmental, social, and governance (ESG) sustainability requirements.

Learn moreMake your short-term cash work harder with a low-risk portfolio, a Bank of England variable rate, plus flexible access.

Learn moreAdd megatrend themes to your portfolio and gain exposure to the high-growth areas changing our world.

Learn moreChoose a diversified portfolio with a mix of assets that meet environmental, social, and governance (ESG) sustainability requirements.

Learn moreMake your short-term cash work harder with a low-risk portfolio, a Bank of England variable rate, plus flexible access.

Learn moreFrom digital advice to one-to-one support with a Dedicated Qualified Wealth Manager, our Wealth tiers are designed to give you the right level of guidance as your investment needs grow.

Trust is earned, not given. If you’re still unsure about Moneyfarm, discover what our clients are saying about us on Trustpilot.

Management fees are charged on your invested amount. You’ll also incur average fund costs (around 0.16% per year) and market spread effects (up to 0.05% per year).

The platform fee applies to all Wealth assets combined. VAT included where applicable.

Explore the performance of our portfolios over time. View overall trends and the performance for specific years.

Explore the full asset breakdown of our seven portfolios – from lower risk to higher risk – by asset type, sector and geography. Use the toggle to switch between Classic and ESG portfolio types.

With our Thematic Investing option, you can add growth themes to your portfolio to invest in megatrends like technological innovation, sustainability and changes in society.

Bastian automatically generates a quarterly portfolio analysis for Wealth clients, available to view directly in the app. Need an update straight away? Generate an on-demand report in seconds, giving you a clear, instant overview of how your portfolio is performing.

*The AI report is an informational support tool and does not replace personalised advice.

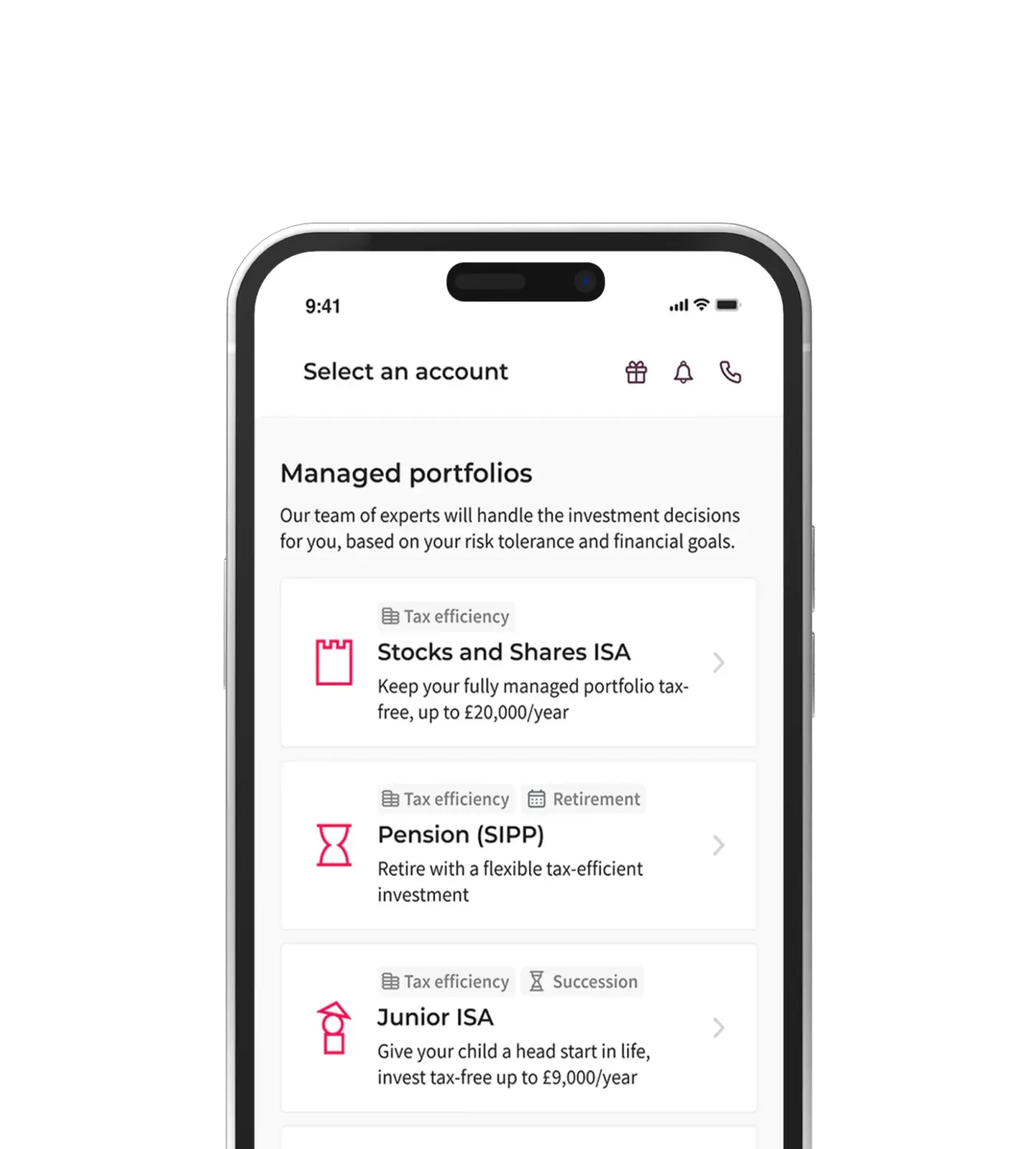

Choose an investment solution or let our questionnaire guide you.

Discover the option best suited to your objectives and needs.

Start your investing journey with our experts by your side.

A Stocks and Shares ISA is an Individual Savings Account that acts as a tax wrapper around your investments. You can invest up to the annual ISA allowance set by the UK government each tax year, either entirely into a Stocks and Shares ISA or split across different ISA types.

Within this account, you can typically invest in:

The key benefit is that any capital growth, dividends or interest generated within the ISA are free from UK tax. You also don’t need to declare ISA investments on your tax return.

When you open a Stocks and Shares ISA, you deposit money into the account and choose how to invest it. Depending on the provider, you may select your own investments or opt for a professionally managed portfolio aligned to your goals and risk appetite.

Your returns depend on how your investments perform. Over time, markets have historically delivered stronger returns than cash, but this comes with fluctuations along the way. The value of your portfolio can go down as well as up, particularly in the short term.

For this reason, a Stocks and Shares ISA is generally considered more suitable for medium to long-term goals (typically five years or more).

Investing outside an ISA means you may be liable for Capital Gains Tax on profits and Dividend Tax on income, depending on your circumstances and annual allowances.

A Stocks and Shares ISA removes that complexity. Its benefits include:

By protecting your returns from tax year after year, an ISA allows more of your money to remain invested and potentially grow over time.

To open a Stocks and Shares ISA, you must:

You can only pay into one Stocks and Shares ISA per tax year, but you can transfer existing ISA savings from previous years to a new provider without losing your tax-free status. Transfers must be completed through the official ISA transfer process.

If you already hold savings in a Cash ISA, you can transfer those funds into a Stocks and Shares ISA if you decide to move from saving to investing.

All investments carry risk. The value of your portfolio may fall, particularly during periods of market volatility. However, time plays a critical role in managing investment risk.

Historically, the longer you stay invested, the greater the opportunity to recover from short-term market downturns. This is why a Stocks and Shares ISA is typically suited to long-term goals such as retirement planning, future property purchases or building general wealth.

Diversification is another important factor. Spreading investments across different asset classes, sectors and regions can help reduce exposure to any single area of the market.

For investors who prefer a structured approach, professionally managed portfolios can help align investment strategy with individual risk tolerance and financial objectives.

The main difference between a Cash ISA and a Stocks and Shares ISA lies in risk and return potential.

A Cash ISA offers stability and capital security, but returns are typically limited to prevailing interest rates. A Stocks and Shares ISA exposes your money to market performance, meaning higher potential growth — but also greater short-term volatility.

Many investors choose to use both as part of a broader strategy, holding cash for short-term needs while investing for longer-term growth.

Your choice depends on your goals, timeframe and comfort with investment risk.

Each tax year, you receive a new ISA allowance. If you don’t use it, it cannot be carried forward. For long-term investors, consistently using this allowance can help build a substantial tax-efficient portfolio over time.

Regular investing — for example, through monthly contributions — can also help smooth out market fluctuations by spreading your investment across different market conditions. This approach, often referred to as pound-cost averaging, reduces the risk of investing a large lump sum at the wrong time.

By combining disciplined contributions with a long-term perspective, a Stocks and Shares ISA can become a powerful wealth-building tool.

A Stocks and Shares ISA may be suitable if you:

Unlike pensions, ISAs allow you to withdraw money at any time without tax charges (though market conditions may affect value). This flexibility makes them attractive for a wide range of financial goals.

A Stocks and Shares ISA offers a balance of flexibility, tax efficiency and growth potential. While investments involve risk, a well-structured and diversified approach — aligned to your goals — can help you make the most of your money over time.

By taking advantage of the ISA wrapper and maintaining a long-term mindset, you give your investments the opportunity to grow without the drag of unnecessary taxation.

As always, it’s important to ensure your investment choices reflect your financial objectives and risk tolerance. With the right strategy in place, a Stocks and Shares ISA can play a central role in building your financial future.

Add megatrend themes to your portfolio and gain exposure to the high-growth areas changing our world.

Sign in

By making an investment, your capital is at risk. The value of your Moneyfarm investment depends on market fluctuations outside of our control and you may get back less than you invest. Past performance is no indicator of future performance. The tax treatment of a Moneyfarm Stocks and Shares ISA and a Moneyfarm Pension depends on your individual circumstances and may be subject to change in the future. You should seek financial advice if you are unsure about investing.

©2026 MFM INVESTMENT Ltd

Registered office: 90-92 Pentonville Road, London N1 9HS | Registered in England and Wales Company No. 09088155 | Telephone number: +44 (0)20 3745 6991 | VAT No. 467458154

Moneyfarm is a trading name of MFM Investment Ltd, which is authorised and regulated by the Financial Conduct Authority (FCA Firm Reference Number: 629539)

Authorised and regulated by the Financial Conduct Authority as an Investment Advisor and Investment Management Company - Authorisation no. 629539

This company meets high standards of social and environmental performance, transparency and accountability.

Moneyfarm uses an encrypted connection to protect your data.

From 6 April 2016 onwards, investors have been able to withdraw money from a Cash ISA or a Stocks & Shares ISA and put it back in without losing that part of their allowance, provided they do so within the same tax year.

At Moneyfarm, this means that any disinvestment (withdrawal) will effectively top up your available ISA allowance for the current tax year, allowing you to reinvest those funds at a later date without eroding your annual limit. Find out more about Flexible ISAs.

Take a look at our handy guide to see the different types of ISAs you can select so that you can choose the best one depending on your needs and situation.

Different investment accounts are suited to different financial goals - learn more about ISAs and SIPPs with our guide.

A Stocks and Shares ISA helps protect your money from inflation and could help you hit your long-term financial goals. On top of this, any money is protected in a tax-free wrapper.

A Stocks & Shares ISA is often used for goals five years away, or more. As markets move up as well as down, there’s an opportunity to grow your money, and often this can help to protect you from inflation risk.

At Moneyfarm we build portfolios with a diverse range of assets based on your investor profile and time horizon to ensure you’re comfortable with any losses, whilst also aiming to deliver long-term returns.

No, we do not offer the Help-to-Buy or Lifetime ISA.

Yes we do! Check out our Cash ISA page for more information.

ISAs have generous tax benefits that can help you maximise your investment returns.

When you invest in an ISA, you’re not charged Capital Gains Tax (CGT) on any profit you make when you sell your investments and withdraw money from your account. Everyone has an annual CGT exemption allowance of £3,000 in the 2024/25 financial year. You’ll be charged CGT on any profit made above this annual allowance if you didn’t invest in an ISA.

Any losses made on your investments in your Stocks & Shares ISAs can’t be used to offset capital gains on your other investments.

ISAs also protect any income from your investments in your tax-free wrapper.

Outside of an ISA, you don’t pay tax on the first £500 of dividends you get in the 2024/2025 tax year. Above this allowance, you pay tax of 8.75-39.35%, depending on your income tax band. If you invest in an ISA, you don’t pay a thing.

The tax treatment of a Moneyfarm Stocks & Shares ISA depends on your individual circumstances and may be subject to change in the future.

To open a Stocks & Shares ISA you must be at least 18 years old and must be a UK resident for tax purposes.

You can withdraw money from your ISA whenever you need to, without it impacting your ISA allowance from that tax year. Moneyfarm does not charge you to withdraw from your ISA, as we know how important it is that you have flexible access to your investments. However, the longer you can keep your money invested, the more you can expect your money to grow to help you have a more financially secure future. Learn how to withdraw your money from a Stocks and Shares ISA

This tax year you can invest up to £20,000 in your ISA. The tax year runs from 6 April until 5 April the following year and that’s when your ISA allowance automatically refreshes.

You can pay your whole allowance of £20,000 into a Stocks and Shares ISA, a Cash ISA, or a combination of the two. Even if you have an ISA elsewhere, you can still open a Stocks and Shares ISA with Moneyfarm, and you can also transfer over an old ISA to your new Moneyfarm account. You can choose between making a lump sum investment, and/or making regular contributions throughout the tax year. Your Moneyfarm ISA is flexible to suit you. Your annual ISA allowance expires at the end of the tax year and any unused allowance will be lost. It’s a case of ‘use it or lose it’, as your allowance can’t be rolled into the next year. With Moneyfarm, you can invest more than the ISA allowance, for example, with a General Investment Account, but any investments outside the ISA wrapper won’t be sheltered from tax. Find out more about how much you can put in your ISA.

Yes we do! Check out our Junior ISA page for more information.

Pension

Products