Unlock your wealth potential with our General Investment Account.

Professional management, personalised investment strategies, and expert consultants by your side.

Professional management, personalised investment strategies, and expert consultants by your side.

Investments can go down in value as well as up, and you may get back less than you put in. See our full risk disclosure for details.

Discover the key benefits of our General Investment Account:

No caps on how much you can invest.

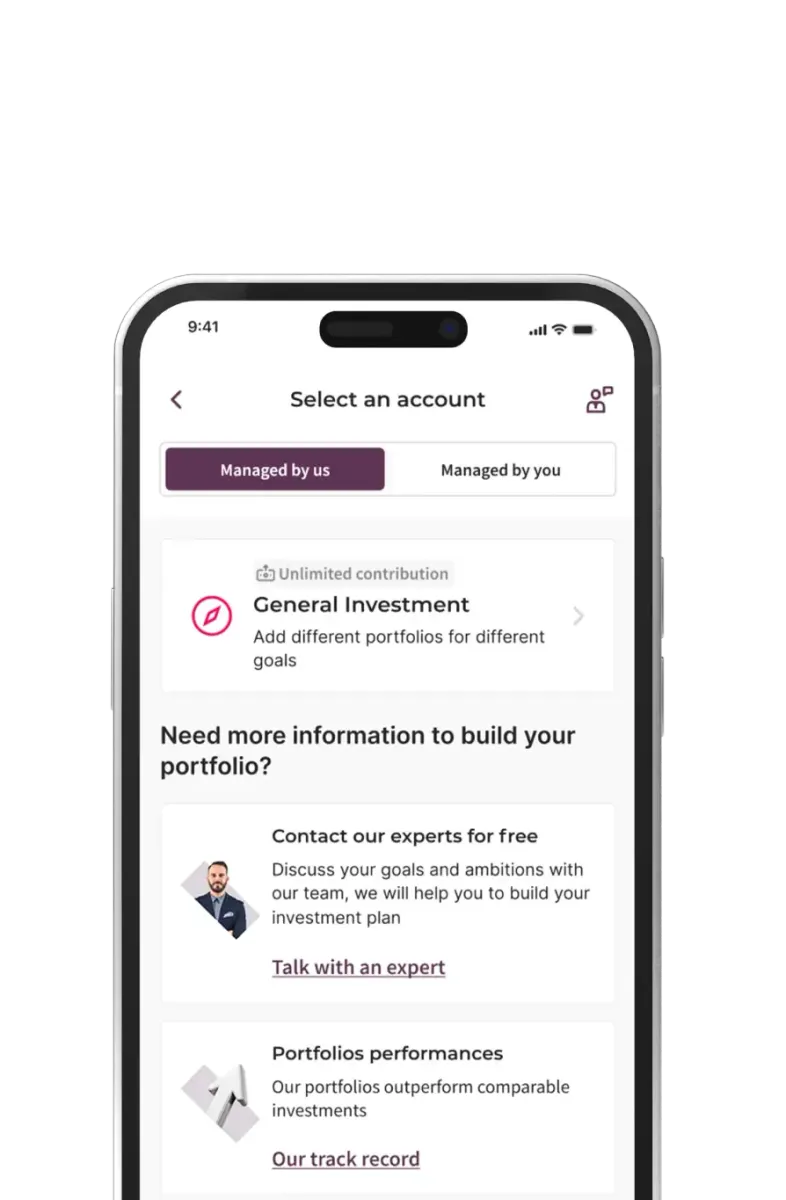

Choose a Managed GIA to benefit fully from our expertise, or build and manage your own portfolio with a DIY GIA.

Choose a Managed GIA if you want our experts to guide you through the portfolio creation process and manage your investments for you. Choose a DIY GIA if you want to choose your own investments and self-manage your portfolio.

Matched to you

Get matched with an expertly built, fully managed, ready-to-go portfolio. Or for a simpler, low-cost approach, choose a fixed allocation portfolio.

Enhanced strategies

Level up your Moneyfarm experience with different investing strategies – ESG, Thematic Investing, or Smart Yield, our smart, short-term investment solution.

Experts at your side

Our dedicated consultants are available at your disposal, ensuring you achieve your investment goals with confidence.

Transparent pricing

Enjoy simple, clear and transparent fees. Set up your portfolio for free. Learn more

Open a Managed GIA

Direct market access

Choose from 1,000+ assets including stocks, ETFs, bonds, and mutual funds.

Guided investment experience

Shape your strategy backed by our team’s market insights and experience. Discover investment themes with our curated asset collections.

Personalise your portfolio

Create a portfolio in line with your values and goals, one investment at a time. All with a comprehensive view of your investments for effective decision-making.

Matched to you

Get matched with an expertly built, fully managed, ready-to-go portfolio. Or for a simpler, low-cost approach, choose a fixed allocation portfolio.

Enhanced strategies

Level up your Moneyfarm experience with different investing strategies – ESG, Thematic Investing, or Smart Yield, our smart, short-term investment solution.

Experts at your side

Our dedicated consultants are available at your disposal, ensuring you achieve your investment goals with confidence.

From digital advice to one-to-one support with a Dedicated Qualified Wealth Manager, our Wealth tiers are designed to give you the right level of guidance as your investment needs grow.

Trust is earned, not given. If you’re still unsure about Moneyfarm, discover what our clients are saying about us on Trustpilot.

Management fees are charged on your invested amount. You’ll also incur average fund costs (around 0.16% per year) and market spread effects (up to 0.05% per year).

The platform fee applies to all Wealth assets combined. VAT included where applicable.

Explore the performance of our portfolios over time. View overall trends and the performance for specific years.

Explore the full asset breakdown of our seven portfolios – from lower risk to higher risk – by asset type, sector and geography. Use the toggle to switch between Classic and ESG portfolio types.

With our Thematic Investing option, you can add growth themes to your portfolio to invest in megatrends like technological innovation, sustainability and changes in society.

Simply input how much you’re thinking of investing initially, how much you might contribute regularly, and for how long.

Bastian automatically generates a quarterly portfolio analysis for Wealth clients, available to view directly in the app. Need an update straight away? Generate an on-demand report in seconds, giving you a clear, instant overview of how your portfolio is performing.

*The AI report is an informational support tool and does not replace personalised advice.

On your own or with help from one of our consultants.

A General Investment Account (GIA) is a straightforward and flexible way to invest in the financial markets outside of tax-wrapped accounts such as ISAs or pensions. If you’ve already used your annual ISA allowance (or you want unrestricted access to your money) a GIA can offer a practical solution.

Unlike pensions or ISAs, a General Investment Account does not have contribution limits or withdrawal restrictions. This makes it particularly attractive for investors who want full flexibility over how much they invest and when they access their funds.

A General Investment Account is a standard investment account that allows you to buy and hold assets such as:

It works in a similar way to an ISA or pension in terms of investment access, but it does not provide the same tax advantages. This means that any income or capital gains generated within the account may be subject to tax, depending on your personal circumstances.

Because there is no annual contribution cap, a GIA can be useful for investing larger sums or continuing to invest once ISA allowances have been fully used.

Opening a GIA allows you to deposit money and allocate it across a range of investments. The value of your account will fluctuate based on market performance.

You can typically:

This flexibility makes GIAs suitable for medium- to long-term financial goals where accessibility is important.

However, since the account is not tax-sheltered, it’s important to understand the potential tax implications.

Unlike ISAs or pensions, investments held within a General Investment Account are not protected from tax.

You may be liable for:

Capital Gains Tax (CGT)

If you sell investments for a profit above the annual Capital Gains Tax allowance, you may need to pay CGT on the gain.

Dividend Tax

Dividends received from shares or equity funds may be subject to Dividend Tax if they exceed the annual dividend allowance.

Income Tax

Interest generated from bond holdings may be subject to Income Tax above your Personal Savings Allowance.

The exact tax treatment depends on your overall income and personal allowances. Some investors use a GIA strategically alongside tax-efficient accounts, carefully managing gains and income to remain within annual thresholds.

Tax rules can change, and individual circumstances vary.

A General Investment Account may be appropriate if you:

For example, if you are building wealth for a property purchase, future business opportunity or general capital growth, a GIA can provide adaptable access to your investments.

The main difference between a GIA and an ISA lies in tax treatment.

An ISA offers tax-free growth and income, but is subject to an annual contribution limit. A GIA has no contribution cap but does not provide tax sheltering.

Many investors use both:

This combination can help maximise tax efficiency while maintaining flexibility.

A General Investment Account typically offers access to a broad range of asset classes, including equities, fixed income and diversified portfolios.

Because there are no structural restrictions on withdrawals, GIAs are often used for goals that may arise before retirement age.

As with any market-based investment, the value of assets can go down as well as up. Diversification (spreading investments across asset types, sectors and regions) can help manage risk within the portfolio.

A GIA is generally more suited to medium- and long-term investing rather than short-term cash storage. While funds can be withdrawn at any time, market volatility may affect the value of your investments when you decide to access them.

Investors often align their portfolio strategy within a GIA according to:

A disciplined investment approach and regular portfolio reviews can help ensure your GIA remains aligned to your evolving objectives.

For many investors, a GIA plays a complementary role within a wider financial plan. It can:

When structured thoughtfully, it can form part of a diversified and flexible investment framework.

A General Investment Account offers freedom: no annual contribution limits, no withdrawal restrictions and broad access to global markets.

While it does not provide the tax advantages of ISAs or pensions, it compensates with adaptability and scale. For investors seeking a versatile investment vehicle (particularly once tax-efficient allowances are maximise) a GIA can be a practical and powerful tool.

As with all investments, capital is at risk and values can fall as well as rise. Understanding the tax implications and aligning your strategy with your long-term goals is essential when investing through a General Investment Account.

Free to open an account

Set up your DIY GIA portfolio for free and get started in no time.

Transparent pricing

Enjoy simple, clear and transparent fees. Set up your portfolio for free. Learn more

Direct market access

Choose from 1,000+ assets including stocks, ETFs, bonds, and mutual funds.

Guided investment experience

Shape your strategy backed by our team’s market insights and experience. Discover investment themes with our curated asset collections.

Personalise your portfolio

Create a portfolio in line with your values and goals, one investment at a time. All with a comprehensive view of your investments for effective decision-making.

Sign in

By making an investment, your capital is at risk. The value of your Moneyfarm investment depends on market fluctuations outside of our control and you may get back less than you invest. Past performance is no indicator of future performance. The tax treatment of a Moneyfarm Stocks and Shares ISA and a Moneyfarm Pension depends on your individual circumstances and may be subject to change in the future. You should seek financial advice if you are unsure about investing.

©2026 MFM INVESTMENT Ltd

Registered office: 90-92 Pentonville Road, London N1 9HS | Registered in England and Wales Company No. 09088155 | Telephone number: +44 (0)20 3745 6991 | VAT No. 467458154

Moneyfarm is a trading name of MFM Investment Ltd, which is authorised and regulated by the Financial Conduct Authority (FCA Firm Reference Number: 629539)

Authorised and regulated by the Financial Conduct Authority as an Investment Advisor and Investment Management Company - Authorisation no. 629539

This company meets high standards of social and environmental performance, transparency and accountability.

Moneyfarm uses an encrypted connection to protect your data.

Moneyfarm offers simplified advice. When you decide to open an account (ISA, SIPP, JISA, or GIA) we will ask you to complete a suitability assessment to assess and recommend a specific portfolio risk level at which you should be trading. We will not advise which product you should subscribe to, but we can guide you and help you understand their respective values, advantages, and the associated investment risks.

The suitability assessment is an online experience and covers your knowledge and experience, financial situation and capacity for loss, risk appetite, and investment time horizon. At the end of the process we recommend either a low, medium, or higher-risk investment portfolio. You can always book an appointment with our investment consultants who can give you more insight into your portfolio composition, the outcome of your suitability assessment, and answer any other questions you might have.

We show your portfolio performance in two different ways and you can toggle between them, called “time-weighted” and “money-weighted” performance.

Time-weighted rate of return (TWRR) tells the performance of your investments over time. It is used to compare the investment returns as it removes the distorting effects of cash inflows and outflows, even as you regularly contribute to your account.

The money-weighted rate of return includes individual cash flows within a period to give an accurate reflection of the return you receive as an individual. We believe this gives you an accurate picture of the true return you received, accounting for your individual cash flows – these could be dividends, account top-ups or disinvestments. If you were to invest – or disinvest – an amount from your portfolio, this impacts the performance number. You can think of this as your portfolio’s “personal performance”. This measure of performance corresponds to a well-known concept called the internal rate of return (IRR).

Customers often confuse these with a “simple return” calculation, which would be found by just dividing your current value by your net contributions, and over time it will be less helpful as every time you invest you will reduce your performance.

All three measures are in theory the same if you only have one cashflow.

If you would like further explanations please speak to our investment adviser team.

A model portfolio is a group of funds that are brought together to target an expected return for a specified amount of risk. Our asset allocation team optimise the asset allocation for each of our model portfolios to ensure they’re suitable for the targets of each portfolio.

Once we have matched you to a portfolio that reflects your investor profile, your investments will be managed by our experts in-line with the model portfolio that suits your profile. For smaller investment amounts, the composition of your portfolio may differ from the model. Please contact us if you would like to know more.

Nothing, but remember it takes a lot of time, knowledge and skill to invest successfully, not to mention the extra capital of trading yourself. It can be especially daunting when you're managing your family's money. It's important you understand your investor profile and make sure your portfolio reflects your tolerance to risk through its asset allocation. Once you've built your portfolio, you'll need to make sure it continues to be suitable for you and your goals. Many investors prefer for the expert to do it for them so they can focus on the important things in life, knowing their wealth manager has their best interests at heart.

At Moneyfarm, we provide a discretionary service, which means we build, manage and rebalance your portfolio on your behalf. After we ask you a series of questions to determine your knowledge, experience, risk appetite and objectives, we match you with the portfolio that best fits your profile. We're regulated to offer this investment advice.

If you don't believe we've matched you to the right portfolio, you can talk to one of our investment advisers who can look at the other options available to you within your suitability constraints.

Yes, you can request to add funds or withdraw from your account at any time of day or night, from your app or desktop. We think it’s important that your investments are flexible to ensure this is a simple, hassle-free process for you. Don’t forget that your portfolio is tied to your financial goals, so it’s always best to contact us if you would like to move a large amount of money. Transferring an ISA or Pension to Moneyfarm is also simple, just follow the steps inside your account and we’ll do the rest. We’ll never charge you a fee for transferring to or away from Moneyfarm, just make sure you do it properly so you don’t lose your tax benefits. Get in touch with our investment consultants if you have any questions.

You’ll need at least £500 (transfer or new contribution), but as a starting point we’d suggest £2,500 or more. We’ll always stick as close to your risk profile as possible, but the more we have to work with, the better we can diversify your portfolio.

If you’re starting with under £5,000, it’s a good idea to set up a monthly Direct Debit of at least £100 to help you reach your goals as quickly as possible.

Free to open an account

Set up your DIY GIA portfolio for free and get started in no time.

Pension

Products