Junior Stocks and Shares ISA.

Give your child the financial head start they deserve with our expertly managed Junior ISA (JISA). Invest up to £9,000 a year with tax-free returns until your child turns 18.

Give your child the financial head start they deserve with our expertly managed Junior ISA (JISA). Invest up to £9,000 a year with tax-free returns until your child turns 18.

Investments can go down in value as well as up, and you may get back less than you put in. See our full risk disclosure for details.

The earlier you invest, the more time you give their wealth the chance to grow.

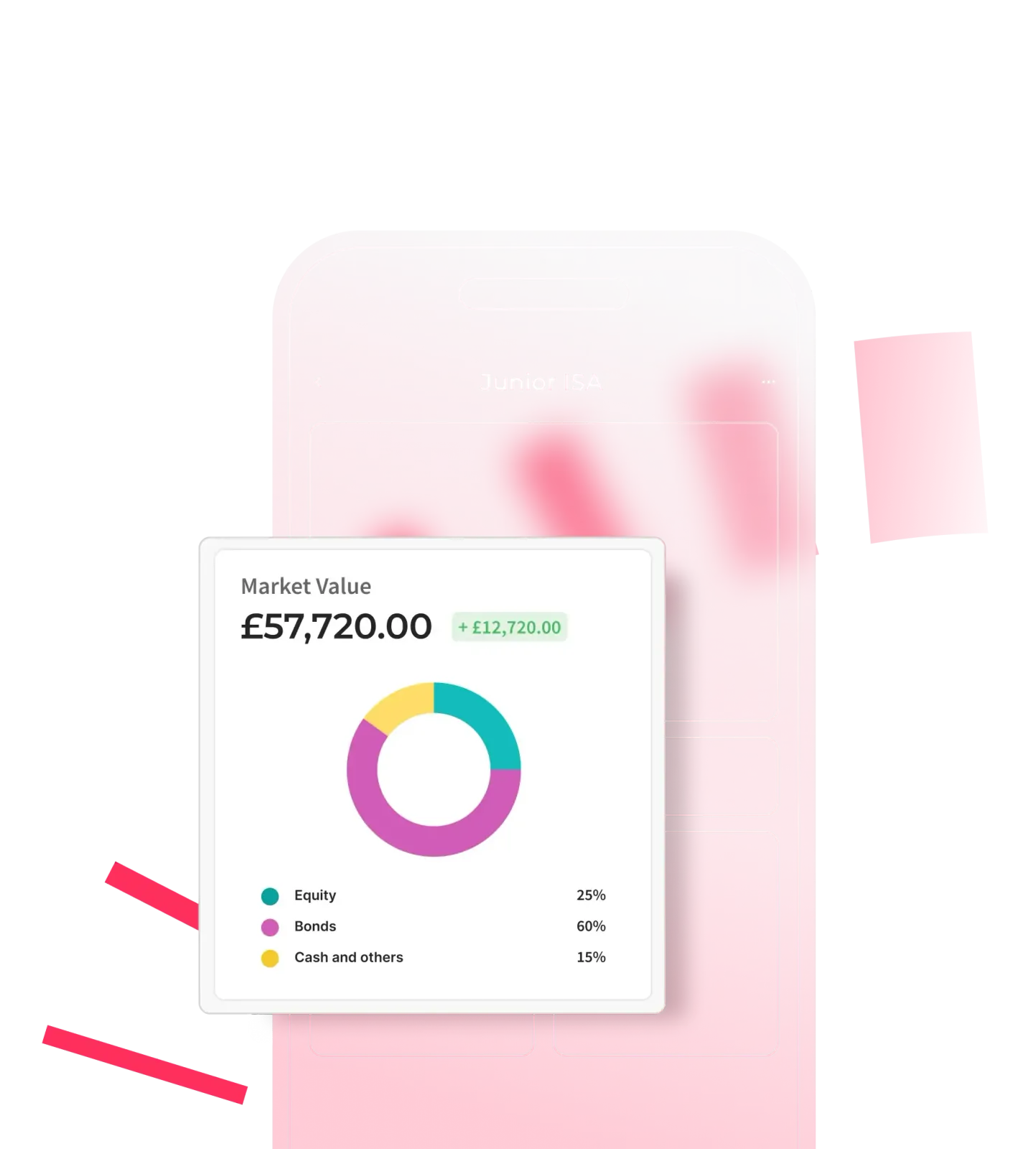

Build their wealth tax-efficiently with a £9,000 tax-free allowance every year.

Opt for a socially responsible JISA with investments that support a positive impact on society and the planet.

Allow family and friends to contribute to your child's financial future.

Easily transfer existing Child Trust Funds or other JISAs to Moneyfarm.

Management fees are charged on your invested amount. You’ll also incur average fund costs (around 0.16% per year) and market spread effects (up to 0.05% per year).

The platform fee applies to all Wealth assets combined. VAT included where applicable.

Explore the performance of our portfolios over time. View overall trends and the performance for specific years.

Explore the full asset breakdown of our seven portfolios – from lower risk to higher risk – by asset type, sector and geography. Use the toggle to switch between Classic and ESG portfolio types.

With our Thematic Investing option, you can add growth themes to your portfolio to invest in megatrends like technological innovation, sustainability and changes in society.

From digital advice to one-to-one support with a Dedicated Qualified Wealth Manager, our Wealth tiers are designed to give you the right level of guidance as your investment needs grow.

Bastian automatically generates a quarterly portfolio analysis for Wealth clients, available to view directly in the app. Need an update straight away? Generate an on-demand report in seconds, giving you a clear, instant overview of how your portfolio is performing.

*The AI report is an informational support tool and does not replace personalised advice.

Choose an investment solution or let our questionnaire guide you.

Discover the option best suited to your objectives and needs.

Start your investing journey with our experts by your side.

A Junior ISA is designed specifically for children. There are two main types:

Each child can have one of each type, or just one. However, the total contributions across both accounts must stay within the annual Junior ISA allowance (set by the UK government and reviewed each tax year).

Anyone can contribute to a Junior ISA – parents, grandparents, relatives or friends – but the total amount paid in cannot exceed the annual limit. All returns, whether interest, dividends or capital gains, are completely free from UK Income Tax and Capital Gains Tax.

The money cannot be withdrawn until the child turns 18. At that point, the Junior ISA automatically becomes an adult ISA, and the child gains full control over the funds.

While a Cash JISA offers certainty, a Stocks and Shares Junior ISA may be more suitable for long-term goals. Because the money is locked in for up to 18 years, many parents choose to invest rather than hold cash. Over longer time horizons, investments have historically offered greater growth potential than cash savings, although returns are not guaranteed and investments can go down as well as up.

A Stocks and Shares Junior ISA allows you to invest in a diversified portfolio of assets such as shares and bonds. Diversification helps spread risk across different markets and sectors, rather than relying on the performance of a single investment.

For parents who want a more hands-off approach, a managed Junior ISA can provide professional portfolio management aligned to your chosen level of risk.

One of the biggest advantages of a Junior ISA is time. The earlier you start contributing, the more opportunity there is for compound growth to work in your child’s favour.

Even modest monthly contributions can grow significantly over 10–18 years. Starting early means you don’t need to invest large sums to build a meaningful fund by adulthood. It also helps spread out contributions over time, making saving more manageable.

Beyond financial growth, opening a Junior ISA can also serve as an educational tool. As children approach 18, it can become an opportunity to introduce conversations around investing, risk and long-term planning.

A parent or legal guardian must open the account on behalf of a child under 18. The child must:

If a child has a Child Trust Fund (CTF), it is possible to transfer it into a Junior ISA, potentially benefiting from a wider range of investment options and competitive management structures.

Once opened, the parent or guardian manages the account until the child turns 16. From age 16, the child can take over management decisions, but withdrawals remain locked until 18.

When your child reaches 18, the Junior ISA automatically converts into an adult ISA. At this stage, they gain full access to the funds and can choose whether to withdraw the money, keep it invested, or continue contributing.

Because the funds become legally theirs, it’s important to consider how and when you introduce them to the concept of long-term financial responsibility. Many parents view the Junior ISA not just as a savings vehicle, but as a way to give their child options — whether that’s funding higher education, supporting a first home deposit, or providing financial flexibility at the start of adult life.

A Junior ISA may be suitable if you:

It may be less suitable if you think you’ll need access to the money before your child turns 18, as withdrawals are not permitted (except in exceptional circumstances).

As with any investment, it’s important to understand your attitude to risk and time horizon. The longer the investment period, the more time there is to ride out market fluctuations.

Choosing how to save or invest for your child is ultimately about planning ahead with intention. A Junior ISA offers a clear framework: tax efficiency, long-term growth potential and a defined purpose.

By starting early, contributing regularly and selecting an investment approach aligned with your goals, you can build a meaningful financial foundation for your child — one that supports their ambitions when they step into adulthood.

Investing involves risk, and the value of investments can go down as well as up. But with a long-term mindset and a disciplined strategy, a Junior ISA can become one of the most effective tools for preparing your child for the opportunities ahead.

Sign in

By making an investment, your capital is at risk. The value of your Moneyfarm investment depends on market fluctuations outside of our control and you may get back less than you invest. Past performance is no indicator of future performance. The tax treatment of a Moneyfarm Stocks and Shares ISA and a Moneyfarm Pension depends on your individual circumstances and may be subject to change in the future. You should seek financial advice if you are unsure about investing.

©2026 MFM INVESTMENT Ltd

Registered office: 90-92 Pentonville Road, London N1 9HS | Registered in England and Wales Company No. 09088155 | Telephone number: +44 (0)20 3745 6991 | VAT No. 467458154

Moneyfarm is a trading name of MFM Investment Ltd, which is authorised and regulated by the Financial Conduct Authority (FCA Firm Reference Number: 629539)

Authorised and regulated by the Financial Conduct Authority as an Investment Advisor and Investment Management Company - Authorisation no. 629539

This company meets high standards of social and environmental performance, transparency and accountability.

Moneyfarm uses an encrypted connection to protect your data.

The Junior ISA allowance is £9,000 per child per tax year (for 2024/25).

Anyone, including parents, grandparents, friends, or family can contribute on behalf of the child, so long as the total contributions don't exceed the annual JISA limit.

Once your child turns 18, their JISA will be put on hold. All the child simply needs to do is create a Moneyfarm account, open an ISA portfolio, and get in touch with us. We’ll migrate their funds from their JISA portfolio to their very own adult ISA portfolio. While the JISA remains on hold, Moneyfarm will continue to manage, rebalance, and apply fees, however, we can’t accept any new contributions (either one-off or recurring), or make any transfers until it has been migrated to an ISA.

Yes - you may transfer Cash JISAs, Stocks & Shares JISAs, and Child Trust Funds to Moneyfarm.

Moneyfarm don’t currently accept customers under the age of 18, so unfortunately we can’t onboard 16--year-olds. Your child will have to wait until they are 18 years old to become the registered contact.

The money in a Junior ISA belongs to the child in all but exceptional circumstances. They cannot withdraw the money until they’re 18 years of age.

As of the 2022/2023 tax year, the annual allowance, or limit, for a JISA is £9,000. Your JISA allowance resets at the start of each new tax year. The tax year ends on 5th April and your allowance, or any unused portion of it, doesn’t carry over to the next tax year, so if you don’t want to lose it, you should use it. Please note, tax treatments depend on your individual circumstances and may change in the future.

As long as you’re a Moneyfarm client, and a parent or legal guardian with parental responsibility, you are eligible. In addition, your child must be both:

However, if your child lives outside the UK, they can open a Junior ISA if both of the following conditions apply:

Yes - Moneyfarm has a minimum one-off investment of £500, which is the same as our minimum threshold for other products, and if you are setting up a Direct Debit you’ll need to set up a monthly contribution of at least £10.

Pension

Products