Earn 3.85% AER* with the Moneyfarm Cash ISA.

Enjoy tax-free growth, daily interest, flexible access, and no fees. All with the security of FSCS protection up to £85,000. - see more

Enjoy tax-free growth, daily interest, flexible access, and no fees. All with the security of FSCS protection up to £85,000. - see more

Your cash is securely held with trusted Qualifying Money Market Funds managed by carefully selected and regulated financial institutions These are "qualifying" because they meet certain regulations that allow them to be considered as cash equivalents.

*Variable rate correct as at 22/05/2026. Subject to conditions and ISA rules.

A smarter way to save - combining flexibility, security, and tax-free benefits to help you make the most of your money.

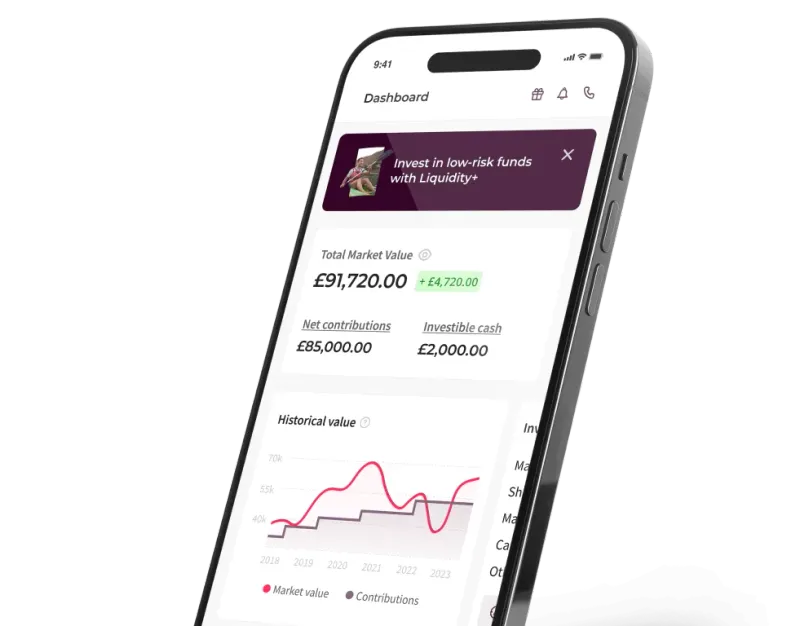

Watch your savings grow every day with tax-free interest applied daily.

Withdraw up to three times a year without impacting your rate, and top up anytime, fee-free.

Your cash is held with trusted partners and safeguarded with FSCS protection up to £85,000.

Consolidate your savings with no transfer fees, making it simple to manage all your ISAs in one place.

Watch your savings grow every day with tax-free interest applied daily.

Withdraw up to three times a year without impacting your rate, and top up anytime, fee-free.

Enjoy tax-free growth with a variable interest rate that rewards you even more in your first year.

Daily interest calculation

Your interest is calculated daily, so you can see your savings growing tax-free.

Boosted first-year rate

Enjoy a higher return with our exclusive bonus rate for the first 12 months, maximising your savings early on.

Your interest is calculated daily, so you can see your savings growing tax-free.

Enjoy a higher return with our exclusive bonus rate for the first 12 months, maximising your savings early on.

Standard rate for your 1st year *

3.85%**

Standard rate after your 1st year

3.55%**

After the 3rd withdrawal in a year

3.55%**

*500 min. balance; New customers rate 3.85%; Existing customers opening a new Cash ISA rate: 3.55% AER (variable); Transfers included; Terms and conditions apply.

**Variable rate correct as at 22/05/2026. Our Cash ISA interest rate is variable and linked to the secure and protected Qualifying Money Market Fund (QMMF) your money is held in. The interest rate may change immediately and will be updated on this page. Subject to conditions and ISA rules.

With the Moneyfarm Cash ISA, you can withdraw funds whenever you need, without penalties - perfect for unexpected expenses or extra peace of mind. Your savings remain flexible and there if you need them.

To maintain the bonus rate, keep at least £500 in your account and limit withdrawals to three per year.

Your savings are safeguarded by the Financial Services Compensation Scheme (FSCS), providing protection of up to £85,000 per eligible person, per bank. This government-backed scheme ensures peace of mind for your hard-earned money, even in the unlikely event of a provider’s failure.

FSCS protection does not cover changes in investment value due to market fluctuations.-See here for more details.

Switching to Moneyfarm is quick, easy, and completely free. Track your transfer every step of the way, with our expert support team ready to assist whenever you need. And remember, anything transferred is outside of the £20,000 annual allowance - so you can transfer anytime.

A Cash ISA (Individual Savings Account) is a savings account available to UK residents aged 18 or over. It works in a similar way to a traditional savings account, but with one key difference: the interest you earn is not subject to Income Tax.

Each tax year, the UK government sets an annual ISA allowance, which is the maximum amount you can contribute across all your ISAs combined (Cash ISA, Stocks and Shares ISA, Innovative Finance ISA, and Lifetime ISA). You can choose to allocate all or part of this allowance to a Cash ISA.

Once money is placed into a Cash ISA, any interest generated is protected from tax year after year, helping your savings grow more efficiently over time.

Opening a Cash ISA is simple. You deposit money into the account, and the provider pays interest on your balance. The key advantage is that this interest is tax-free.

You can usually choose between:

The right option depends on your financial goals and how quickly you may need access to your savings. If flexibility is important, easy access accounts may be suitable for you. If you are confident you won’t need the money for a fixed period, a fixed-rate option may offer more certainty.

Many savers ask whether a Cash ISA is still worthwhile given the Personal Savings Allowance (PSA). The PSA allows basic rate taxpayers to earn a certain amount of savings interest tax-free each year, with lower allowances for higher-rate taxpayers.

However, a Cash ISA can still offer advantages:

If you have substantial savings or expect your interest earnings to exceed your Personal Savings Allowance, a Cash ISA can provide valuable protection. It can also be useful if your tax band changes in the future.

To open a Cash ISA, you must:

You can only open and pay into one Cash ISA per tax year, but you can transfer previous years’ ISA savings to a new provider if you find a more competitive rate or better features.

ISA transfers must be completed through the official transfer process to ensure your tax-free status is maintained. Withdrawing the money yourself and redepositing it could affect your allowance.

The ISA allowance resets at the start of each new tax year (6 April). If you don’t use it, you lose it — unused allowance cannot be carried forward.

For this reason, many savers aim to make full or partial use of their ISA allowance annually, even if they initially hold funds in cash before later deciding to invest.

Using your allowance strategically can help build a growing tax-efficient savings pot over time.

A Cash ISA may be appropriate if you:

It is particularly suited to those who prioritise capital preservation over investment growth. Unlike Stocks and Shares ISAs, a Cash ISA does not expose your money to market fluctuations. Your capital is not at risk from market movements (although inflation can reduce the real value of cash over time).

If your goal is long-term growth and you are comfortable with investment risk, you may wish to consider whether combining cash savings with investment options better suits your overall financial plan.

Depending on the type of Cash ISA you choose, you may be able to access your money whenever you need it, or you may agree to lock it away for a fixed period.

Some providers also offer flexible ISAs, which allow you to withdraw and replace money within the same tax year without affecting your annual allowance. This feature can be useful if you anticipate temporary cash flow needs.

Before opening an account, it’s important to check withdrawal rules, interest structures and any applicable conditions.

A Cash ISA offers a combination of simplicity, tax efficiency and security. While returns may vary depending on interest rates, the tax-free wrapper ensures that everything you earn stays yours.

For many savers, a Cash ISA forms part of a broader financial strategy — balancing accessible savings with longer-term investments. By understanding how the allowance works, comparing access options, and aligning your account choice with your goals, you can use a Cash ISA as a practical building block in your overall financial planning.

As with any financial product, it’s important to review your needs regularly and ensure your savings approach reflects your evolving circumstances.

Your cash is held with trusted partners and safeguarded with FSCS protection up to £85,000.

Consolidate your savings with no transfer fees, making it simple to manage all your ISAs in one place.

Sign in

By making an investment, your capital is at risk. The value of your Moneyfarm investment depends on market fluctuations outside of our control and you may get back less than you invest. Past performance is no indicator of future performance. The tax treatment of a Moneyfarm Stocks and Shares ISA and a Moneyfarm Pension depends on your individual circumstances and may be subject to change in the future. You should seek financial advice if you are unsure about investing.

©2026 MFM INVESTMENT Ltd

Registered office: 90-92 Pentonville Road, London N1 9HS | Registered in England and Wales Company No. 09088155 | Telephone number: +44 (0)20 3745 6991 | VAT No. 467458154

Moneyfarm is a trading name of MFM Investment Ltd, which is authorised and regulated by the Financial Conduct Authority (FCA Firm Reference Number: 629539)

Products

Authorised and regulated by the Financial Conduct Authority as an Investment Advisor and Investment Management Company - Authorisation no. 629539

This company meets high standards of social and environmental performance, transparency and accountability.

Moneyfarm uses an encrypted connection to protect your data.

Your Cash ISA is invested in qualifying money market funds and is protected under the Financial Services Compensation Scheme (FSCS) investment protection, not the deposit protection scheme. This means you may be entitled to compensation of up to £85,000 if MFM Investment Ltd were to fail and you suffer a financial loss as a result. FSCS protection does not cover losses from market performance.

Funds typically appear in your account within 1–2 working days after we receive them.

We update this page whenever the rate changes. While we do not currently send proactive notifications, we are exploring ways to improve this.

Interest starts accruing from the next working day after your funds have been received and cleared.

Yes, withdrawing money is quick and easy from your Moneyfarm Cash ISA, with withdrawals into your Moneyfarm account paid in 1 working day. Just head to your Cash ISA in the Moneyfarm app to request the amount you want to withdraw from your ISA.

Please note that the Moneyfarm Cash ISA is a flexible ISA, which means you can withdraw and replace money within the same tax year without affecting your annual ISA allowance. However, to qualify for the standard interest rate, you’ll need to ensure you don’t make more than 3 withdrawals in a single year. If you withdraw more than 3 times in a year, the interest rate on your Cash ISA will drop to our standard rate.

A money market fund (MMF) is a type of fund that is trusted by banks, other financial institutions and large companies to keep their money safe and accessible, while giving them a return.

A qualifying money market fund (QMMF) is a type of money market fund that is approved to hold client money, for example Cash ISA savings. What makes it “qualifying” is that the QMMF must meet higher regulatory standards than other MMFs.

Yes. Our Cash ISA has a variable rate, which means the rate can go up or down according to market conditions (largely driven by any changes in the Bank of England base rate). If we have to make a change to the rate we offer in the future, we’ll let customers know as soon as possible.

Note that the rate for our Cash ISA can also drop to a lower rate if the balance for a customer’s new contributions falls below £500 or they make more than 3 withdrawals in a year.

ISA transfers can take up to 21 days for Cash ISAs and up to 30 days for Stocks & Shares ISAs. This timeline also applies to Etoro/Moneyfarm ISA transfers. The exact duration depends on how quickly your current provider processes the transfer.